Rush Zarrabian, CFA®

Corbett Road

Managing Partner, Portfolio Manager

—

December 17, 2024

Summary

-

Consumer balance sheets remain healthy, with manageable debt levels and ample room for further spending to support economic growth. Coupled with a relatively young economic cycle, this suggests continued room for expansion in 2025.

-

While proposed tariffs could drive higher prices for certain goods, their overall economic impact may be limited as U.S. consumers now spend far more on services than goods.

-

The Fed is expected to cut rates by 0.25% this week, but will proceed cautiously in 2025, balancing inflation risks with economic support. Meanwhile, ongoing easing from central banks around the world provides a favorable backdrop for the global economy.

-

The S&P 500 is on track to close 2024 with gains exceeding 20% for the second consecutive year—a rare feat. Historically, similar strength has been followed by an average gain of 12% in the third year.

-

Our current microcast™ signal sits at a neutral allocation, down from last month’s aggressive stance. Overall, these signals remain positive and support a favorable outlook for our tactical investment strategies.

THE ECONOMY IS ENTERING 2025 ON SOLID FOOTING

The United States is a consumer-driven economy, and the financial health of consumers remains solid. We think this bodes well for the overall economy next year.

While concerns about the size of the federal debt burden often dominates discussions, the financial situation of households presents a much more favorable picture.

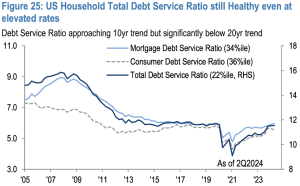

One key indicator, the household debt service ratio—which measures the percentage of total debt payments to total disposable income—shows that consumers are managing their financial obligations effectively. This reflects a healthy balance between income levels and debt payments, supporting continued consumer spending, a critical engine of economic growth (chart from JP Morgan):

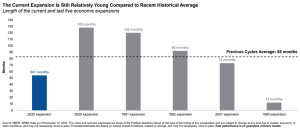

Measured in months, the current economic cycle is also relatively young. By comparison, the last expansion ran from 2009 to 2020 and likely would have continued if not for the pandemic-induced downturn. As of now, the current expansion is just under five years old, meaning there may still be room for further growth (chart from Morgan Stanley):

TODAY’S ECONOMY IS LESS VULNERABLE TO TARIFFS

Tariffs are back in focus, as the incoming administration has signaled an intent to raise tariffs on multiple countries next year. However, the extent to which these statements reflect actual policy versus pre-negotiation tactics remains unclear. For now, it’s prudent to reserve judgment and monitor how these policies develop.

What is clear is that new tariffs imposed on goods are likely to drive higher prices for consumers. Examining historical inflation data, goods subject to tariffs during the first Trump administration experienced price increases that exceeded those of other non-tariffed categories. The chart below is from Goldman Sachs underscores this disparity, highlighting the connection between tariffs and inflation in specific consumer goods.

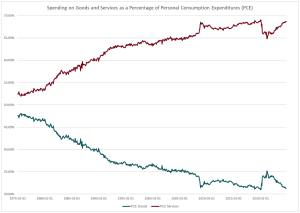

While escalating tariff policies may affect consumer spending on certain items, it’s important to note that U.S. consumers allocate a much larger share of their budgets to non-tariffed, service categories, such as housing and healthcare, than to discretionary goods (data from St. Louis Fed):

U.S. consumer spending habits have shifted dramatically over the decades. In the 1970s, spending was evenly split between goods and services. Today, consumers spend roughly twice as much on services as on goods.

While tariffs could pose challenges—especially for those in impacted industries and lower-income households—the shift in consumer spending towards services suggests the broader economic ripple effects are likely to be contained and less significant than many fear.

THE FED IS UNLIKELY TO AGGRESSIVELY CUT RATES NEXT YEAR

The Federal Reserve is expected to lower interest rates by 0.25% on December 18th but will likely signal caution against pursuing aggressive cuts in 2025. This measured stance reflects the Fed’s intent to assess the potential inflationary pressures stemming from anticipated tariffs and pro-growth policies under the incoming administration.

Still, the Federal Reserve may be overestimating current inflation rates. Real-time housing data indicates core inflation could already be below the 2% target when adjusted for current housing market conditions. If this trend continues, it may provide the Fed with greater flexibility to reduce rates without reigniting inflation. This dynamic will be crucial in shaping the Fed’s policy trajectory in the coming months.

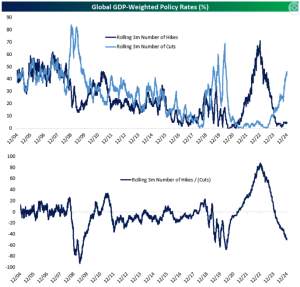

Even if the Fed refrains from further rate cuts in 2025, global central banks have been actively easing monetary policy throughout the year. This collective effort to lower rates should provide a supportive backdrop for the global economy (chart from Bespoke):

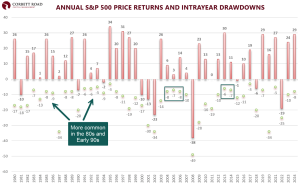

WHAT HAPPENED AFTER TWO STRONG BACK-TO-BACK YEARS?

The stock market is poised to close 2024 on a high note, with the S&P 500 achieving gains exceeding 20% for the second consecutive year. Such robust back-to-back years are rare, occurring only eight times since 1950.

The good news is that this pattern hasn’t historically hindered future performance. In six of the eight instances, the market posted gains in the third year, averaging a 12% increase.

Notably, 2024 delivered substantial gains without experiencing a 10% decline. Consecutive years without a correction have been rare, especially in the 21st century. The last time the market saw two consecutive years without a 10% correction was in 2013 and 2014. While the market may see further gains in 2025, the chances of avoiding a correction next year are relatively low.

While we believe a 10% market decline is more likely next year, it won’t necessarily signal the end of the bull market. Analysis from Ryan Detrick of Carson Group highlights that bull markets often have significant staying power after their third year.

Corrections are a normal part of market behavior and do not always mark the end of an upward trend. If economic fundamentals and corporate earnings remain strong, the bull market may have significant room to continue its run.

In summary, consumers—and by extension, the economy—are entering 2025 in relatively strong shape. While policy uncertainty around tariffs remains a concern, consumer spending today is far more weighted toward services than tariff-eligible goods. Additionally, the economic cycle remains young relative to recent history, and monetary policy has been accommodative—a stark contrast to the aggressive rate hikes of 2022 and 2023. Finally, while the market’s strong performance doesn’t rule out another positive year, investors should prepare for a decline of 10% or more at some point next year.

This is the final Musings of the year. We will publish our 2024 Year in Review next month.

IMPORTANT DISCLOSURES

The chart(s)/graph(s) shown is(are) for informational purposes only and should not be considered as an offer to buy, solicitation to sell, or recommendation to engage in any transaction or strategy. Past performance may not be indicative of future results. While the sources of information, including any forward-looking statements and estimates, included in this (these) chart(s)/graph(s) was deemed reliable, Corbett Road Wealth Management (CRWM), Spire Wealth Management LLC, Spire Securities LLC and its affiliates do not guarantee its accuracy.

The views and opinions expressed in this article are those of the authors as of the date of this publication, are subject to change without notice, and do not necessarily reflect the opinions of Spire Wealth Management LLC, Spire Securities LLC or its affiliates.

All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. macrocastTM and microcastTM are proprietary indexes used by Corbett Road Wealth Management to help assist in the investment decision-making process. Neither the information provided by macrocastTM or microcastTM nor any opinion expressed herein considers any investor’s individual circumstances nor should it be treated as personalized advice. Individual investors should consult with a financial professional before engaging in any transaction or strategy. The phrase “the market” refers to the S&P 500 Total Return Index unless otherwise stated. The phrase “risk assets” refers to equities, REITs, high yield bonds, and other high volatility securities.

Use of Indicators

Corbett Road’s quantitative models utilize a variety of factors to analyze trends in economic conditions and the stock market to determine asset and sector allocations that help us gauge market movements in the short- and intermediate term. There is no guarantee that these models or any of the factors used by these models will result in favorable performance returns.

Individual stocks are shown to illustrate market trends and are not included as securities owned by CRWM. Any names held by CRWM is coincidental. To be considered for investment by CRWM, a security must pass the Firm’s fundamental review process, meet certain internal guidelines, and fit within the parameters of the Firm’s quantitative models.

Spire Wealth Management, LLC is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC, a Registered Broker/Dealer and member FINRA/SIPC. Registration does not imply any level of skill or training.