Rush Zarrabian, CFA®

Corbett Road

Managing Partner, Portfolio Manager

—

May 16, 2024

Summary

-

macrocast™ remains positive and suggests the risk of a recessionary bear market in 2024 remains low. Our current microcast™ signal remains at an aggressive allocation. Both models continue to indicate a generally optimistic outlook for risk assets.

-

Worries about “stagflation” have recently resurfaced due to slower economic growth, but the data suggests these concerns may be overblown. While inflation remains a challenge, it’s trending downwards, and underlying economic activity appears more robust than headline GDP figures indicate.

-

The Misery Index, a combination of the unemployment rate and annual inflation rate, is a helpful tool for assessing the economy. Currently at 7.3%, the index is above pre-pandemic levels but still significantly below its historical average. Although the pace of the decline in inflation data has moderated since last year, the index reflects an economy that remains resilient and stable relative to history.

-

The Federal Reserve faces a challenging decision on whether to lower interest rates before the November 2024 presidential election. With limited opportunities to act, July appears to be the most viable window for a rate cut. Crucially, the Fed must base its decision strictly on economic data, not on political considerations. Its independence and reputation hinge on maintaining this impartiality.

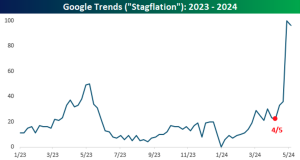

STAGFLATION DEBATE HEATS UP AS INFLATION PERSISTS AND GROWTH SLOWS

After unexpectedly slow economic growth in the first quarter, concerns about “stagflation” resurfaced, as evidenced by a sharp increase in Google searches for the term (chart from Bespoke):

In our view, the US economy is not experiencing stagflation, which is defined as persistently high inflation combined with stagnant economic growth and high unemployment.

First, although core inflation remains high at 3.6% annually as of April, it has decreased from its September 2022 peak of 6.6%. It is also below its five-year average (chart from Atlanta Fed):

Second, while GDP growth in the first quarter was lower than expected, this was largely due to a decline in net exports, a subcomponent of GDP that is notoriously volatile from quarter to quarter. An analysis by economist Ernie Tedeschi, showcases private domestic final purchases (PDFP), a measure of “core GDP” that strips out the volatile components of GDP and focuses on consumption and fixed investment to better measure the underlying growth trend. PDFP indicated much stronger growth last quarter:

Interestingly, this measure of economic activity revealed significantly weaker growth in the second half of 2022, with figures that bordered on recessionary. Since then, private domestic final purchases have increased by 3% or more in four of the last five quarters.

THE MISERY INDEX: A 1970s TOOL FOR TODAY’S ECONOMY

A straightforward method to determine if we are in a stagflationary environment is to consult the Misery Index. This economic indicator, popularized by economist Arthur Okun in the 1970s, sums the unemployment rate with the annual inflation rate. A high Misery Index indicates significant economic hardship, as it captures both high unemployment and a rising cost of living (chart from Ed Yardeni):

While the Misery Index is not a tool for predicting future trends, it provides a valuable snapshot of the economy that can be used to compare current economic conditions to historical periods. Currently, the Misery Index sits at 7.3%, below its long-term average, reflecting a relatively healthy economic environment. Notably, the index is significantly below levels seen throughout the 1970s, the last major period of stagflation.

Excluding the brief period during the pandemic when the index reached 15% due to shutdowns and job losses, the Misery Index recently spiked to heights not seen since the early 2010s. While high unemployment was the primary driver during the 2010s, the latest surge was predominately due to high inflation. The unemployment rate has been below 4% for the past 27 months and remains near 50-year lows.

In short, the Misery Index today does not reflect a stagflationary market environment. The labor market remains healthy, and inflation continues to moderate. Absent a meaningful reacceleration in inflation or a significant increase in unemployment, it’s unlikely we see the Misery Index return to stagflation levels.

THE FED’s PRE-ELECTION DILEMMA: TO CUT OR NOT TO CUT

The Federal Reserve is grappling with the decision of whether to lower interest rates before the November 2024 presidential election. Reducing rates could stimulate the economy and indicate that inflation is under control; however, premature cuts could reinvigorate inflation.

The opportunities to change interest rates are limited. There are only three scheduled Fed meetings before the election—in mid-June, late July, and mid-September.

Currently, the probability of a June rate cut is low according to Fed fund futures, though this could shift if inflation data improves in the next 30 days. As of now, that seems unlikely, and it’s unlikely that rates will be cut in September, just 50 days before Election Day. This scenario leaves July as the only plausible window for a rate cut that would not appear to be politically motivated, underlining the Fed’s commitment to maintaining its independence.

The perception that the Federal Reserve is lowering rates merely to aid the current president’s re-election bid could significantly damage its reputation. The Fed is mandated to remain independent and base its decisions on economic needs rather than political affiliations. However, if inflation continues to ease or if unemployment rises, the Fed will have more substantial data to justify rate cuts. This approach ensures the Fed’s decisions are anchored in economic reality—not political convenience—reinforcing its commitment to impartiality.

In summary, the US economy shows little signs of stagflation. Unemployment remains low, inflation is moderating, and underlying economic growth remains robust. The Misery Index, a stagflation indicator from the 1970s, is slightly above pre-pandemic levels but significantly below historical averages. Meanwhile, the Federal Reserve might have just one chance to cut rates before the election, contingent on inflation declining or unemployment rising.

IMPORTANT DISCLOSURES

The chart(s)/graph(s) shown is(are) for informational purposes only and should not be considered as an offer to buy, solicitation to sell, or recommendation to engage in any transaction or strategy. Past performance may not be indicative of future results. While the sources of information, including any forward-looking statements and estimates, included in this (these) chart(s)/graph(s) was deemed reliable, Corbett Road Wealth Management (CRWM), Spire Wealth Management LLC, Spire Securities LLC and its affiliates do not guarantee its accuracy.

The views and opinions expressed in this article are those of the authors as of the date of this publication, are subject to change without notice, and do not necessarily reflect the opinions of Spire Wealth Management LLC, Spire Securities LLC or its affiliates.

All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. macrocastTM and microcastTM are proprietary indexes used by Corbett Road Wealth Management to help assist in the investment decision-making process. Neither the information provided by macrocastTM or microcastTM nor any opinion expressed herein considers any investor’s individual circumstances nor should it be treated as personalized advice. Individual investors should consult with a financial professional before engaging in any transaction or strategy. The phrase “the market” refers to the S&P 500 Total Return Index unless otherwise stated. The phrase “risk assets” refers to equities, REITs, high yield bonds, and other high volatility securities.

Use of Indicators

Corbett Road’s quantitative models utilize a variety of factors to analyze trends in economic conditions and the stock market to determine asset and sector allocations that help us gauge market movements in the short- and intermediate term. There is no guarantee that these models or any of the factors used by these models will result in favorable performance returns.

Individual stocks are shown to illustrate market trends and are not included as securities owned by CRWM. Any names held by CRWM is coincidental. To be considered for investment by CRWM, a security must pass the Firm’s fundamental review process, meet certain internal guidelines, and fit within the parameters of the Firm’s quantitative models.

Spire Wealth Management, LLC is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC, a Registered Broker/Dealer and member FINRA/SIPC. Registration does not imply any level of skill or training.