Rush Zarrabian, CFA®

Corbett Road

Managing Partner, Portfolio Manager

—

September 17, 2024

Summary

-

macrocast™ score is unchanged from August. macrocast™ remains modestly positive, indicating a low risk of a recessionary bear market. Our current microcast™ signal remains at a neutral allocation. Both models suggest a cautiously optimistic outlook for risk assets, though the risks are more balanced now than they were earlier in the year.

-

The Federal Reserve is set to begin a rate cutting cycle on September 18th. An initial 0.25%-0.50% cut is expected, the first of several over the next year as their attention moves from inflation to a slowdown in employment growth.

-

Despite fears of a potential recession, indicators such as falling oil prices, still-positive job growth, and strong consumer balance sheets suggest that the economy has the underlying strength to achieve a soft landing and avoid a deep downturn.

-

The upcoming U.S. presidential election introduces uncertainty that may lead to short-term market volatility; however, history shows that markets tend to stabilize and often rally once the election outcome is clear, regardless of which party wins.

ANTICIPATING A NEW RATE CUTTING CYCLE

The Federal Reserve is expected to implement its first interest rate cut since 2020 at this week’s meeting, marking a significant shift in monetary policy. An initial reduction of 0.25% seems likely, but the probabilities implied by futures markets suggest a 0.50% cut is also a possibility.

This move follows a series of rate hikes over the past two years, aimed at tackling the highest inflation since the 1980s. Lowering rates now suggests that inflationary pressures have eased, but it also highlights concerns about slowing economic growth and rising unemployment. The Fed aims to boost economic activity and stabilize the job market while maintaining price stability, i.e. support economic growth without triggering a resurgence in inflation. Lower interest rates can boost demand by making borrowing cheaper and encouraging investment. However, if growth becomes too rapid, it could reignite inflationary pressures.

For now, inflation is no longer the primary concern. According to the latest New York Fed Survey, consumer inflation expectations have continued to normalize. This suggests that people are adjusting their expectations and no longer see rising prices as a major, ongoing issue:

ARE RATE CUTS TOO LITTLE TOO LATE?

Some market participants worry the rate-cutting cycle may be coming too late to prevent a recession. They fear the economy has already slowed too much, and delayed cuts could limit their effectiveness in stabilizing growth. On the other hand, the Fed remains confident it can still achieve a soft landing, balancing inflation control with continued economic expansion. The central bank believes its current approach will help the economy avoid a deep downturn without compromising the progress they’ve made on bringing inflation back down towards target levels.

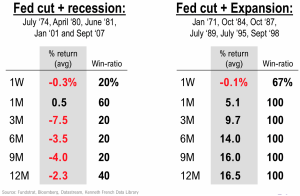

Whether the rate cuts are coming just in time or too late to avoid recession is a crucial distinction for equity markets. A study by Fundstrat shows that when rate cuts coincide with a recession, future returns are generally worse over a 3- to 12-month period. In contrast, when rate cuts occur alongside continued economic expansion, returns have been universally positive in the following months:

In our view, a soft landing is still achievable. The economy is coming from a position of strength, supported by lower oil prices, healthy employment levels, and resilient household balance sheets.

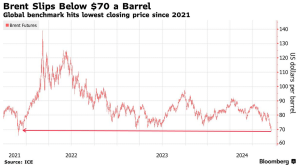

First, oil prices have been falling most of the year. Recessions have historically been preceded by a large increase in oil prices. Today, the opposite is happening. Oil prices recently dropped below $70 a barrel for the first time since December 2021 (chart from Bloomberg):

Second, while the labor market has clearly cooled from the robust rate of growth seen over the past few years, monthly job growth is still positive. Further, initial claims for unemployment—a key, real-time indicator of labor market health—are still low. Absent a significant uptick in job losses, it is unlikely the economy falls into a recession (chart from DataTrek):

Finally, consumers’ balance sheets remain strong. Debt service payments as a percentage of income are near multi-decade lows. Low debt burdens translate into greater flexibility, which could help soften the blow if the broader economy weakens (from St. Louis Fed):

These trends suggest the economy has enough underlying strength to hold up through a moderate slowdown without falling into a recession.

ELECTION SEASON IS HERE, AND THAT MEANS VOLATILITY IS LIKELY

The upcoming U.S. presidential election is undoubtedly a major event, and it’s likely to influence market behavior over the coming months. Elections, by nature, introduce uncertainty, which often leads to short-term volatility as investors weigh the possible outcomes and their impact on policy. This is especially common in the period leading up to the vote, as market participants try to gauge the direction of key policy and regulatory decisions.

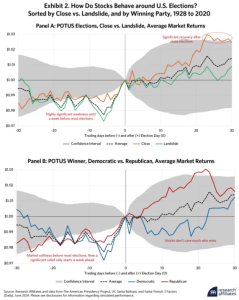

However, there’s reason for optimism once the election outcome becomes clear. Markets tend to stabilize and often rally regardless of the result—whether the race is close or a landslide, and regardless of which party wins the White House. This pattern reflects the fact that markets prefer clarity, and once the uncertainty is resolved, confidence generally improves (chart from Research Affiliates via Bloomberg.com):

In summary, while there are near-term uncertainties in the path of monetary policy normalization and the outcome of the upcoming election—the overall economic data provides reasons for cautious optimism. Lower oil prices, resilient employment figures, and strong consumer balance sheets suggest that the economy is well-positioned to navigate these challenges. If history repeats itself, the market should adapt and thrive post-election, regardless of the outcome.

IMPORTANT DISCLOSURES

The chart(s)/graph(s) shown is(are) for informational purposes only and should not be considered as an offer to buy, solicitation to sell, or recommendation to engage in any transaction or strategy. Past performance may not be indicative of future results. While the sources of information, including any forward-looking statements and estimates, included in this (these) chart(s)/graph(s) was deemed reliable, Corbett Road Wealth Management (CRWM), Spire Wealth Management LLC, Spire Securities LLC and its affiliates do not guarantee its accuracy.

The views and opinions expressed in this article are those of the authors as of the date of this publication, are subject to change without notice, and do not necessarily reflect the opinions of Spire Wealth Management LLC, Spire Securities LLC or its affiliates.

All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. macrocastTM and microcastTM are proprietary indexes used by Corbett Road Wealth Management to help assist in the investment decision-making process. Neither the information provided by macrocastTM or microcastTM nor any opinion expressed herein considers any investor’s individual circumstances nor should it be treated as personalized advice. Individual investors should consult with a financial professional before engaging in any transaction or strategy. The phrase “the market” refers to the S&P 500 Total Return Index unless otherwise stated. The phrase “risk assets” refers to equities, REITs, high yield bonds, and other high volatility securities.

Use of Indicators

Corbett Road’s quantitative models utilize a variety of factors to analyze trends in economic conditions and the stock market to determine asset and sector allocations that help us gauge market movements in the short- and intermediate term. There is no guarantee that these models or any of the factors used by these models will result in favorable performance returns.

Individual stocks are shown to illustrate market trends and are not included as securities owned by CRWM. Any names held by CRWM is coincidental. To be considered for investment by CRWM, a security must pass the Firm’s fundamental review process, meet certain internal guidelines, and fit within the parameters of the Firm’s quantitative models.

Spire Wealth Management, LLC is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC, a Registered Broker/Dealer and member FINRA/SIPC. Registration does not imply any level of skill or training.